A quarter of nationwide auto loans are financed by credit unions, making auto lending a significant component of a credit union’s total loan portfolio. Now with 2022 fast approaching, and vehicle sales reaching pre-pandemic normalcy, credit unions need to rethink their auto lending strategy.

Here are some interesting facts from Filene’s most recent study on credit union auto loans that every CU should know.

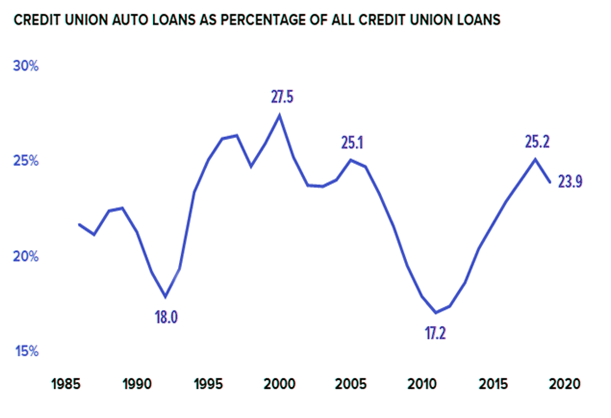

- In the last three decades or so, auto loans have made up between 17% to 27.5% of all loans of any credit union (Figure 1).

- The share of auto loans against credit unions’ total loans has declined since 2018 after reaching a high of 25.2% (Figure 1).

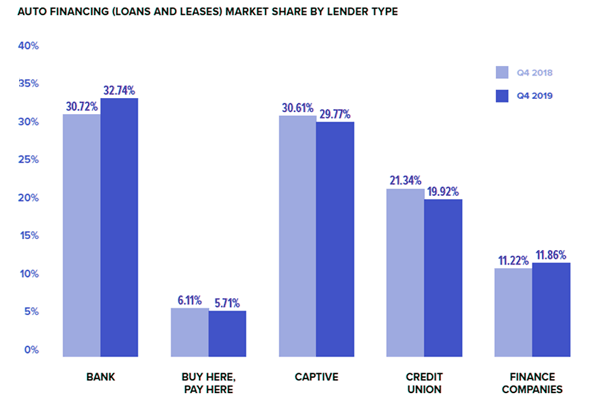

- In Q4 of 2019, banks and captive financing emerged as the topmost choices for consumers to finance their auto loans, while credit unions ranked third. (Figure 2).

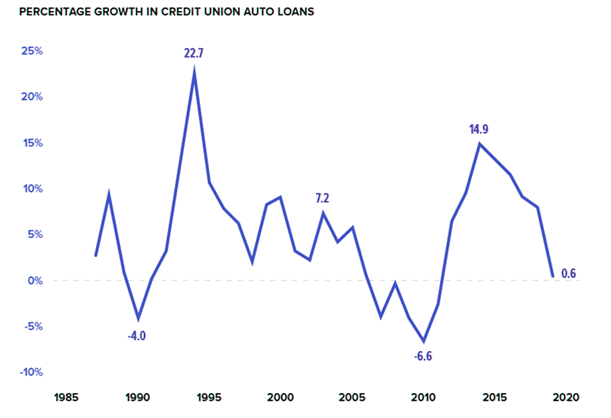

- In 2020, total credit union auto loans witnessed a growth of only 0.6%, significantly down from 14.9% growth from seven years ago (Figure 3).

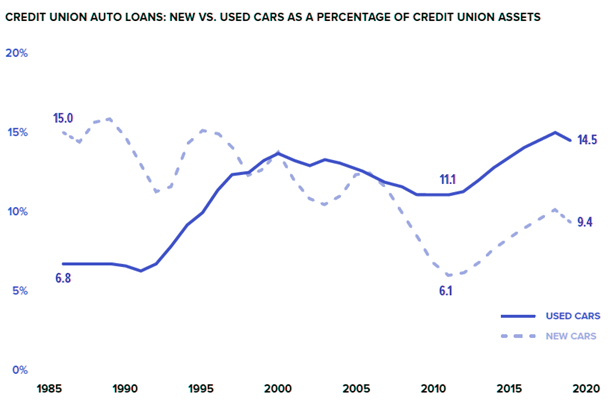

- Credit Unions are strong in the used car category by financing 14.5% of these loans against 9.4% of new car loans (Figure 4).

Figure 1

Figure 2

Figure 3

Figure 4

A major factor contributing to the declining growth rate of auto loans with credit unions, is increased aggressiveness of banks and captives for those loans. This is clear in Figure 2, where we see that banks pushed their share of auto loans by almost 2.02% in Q4 2019 compared to 2018.

It is established that credit unions need to think and act fast to regain their shrinking share of auto loans. So where should the credit unions start? By studying their existing membership data! The current members present a plethora of information about themselves through their current transactional/payment behavior and logged demographic profiles. This information, when mined can uncover opportunities for capturing new auto loans with current members. Let us discuss the 4 ways to achieve this:

- Recapture your members’ auto loans financed elsewhere with competitive rates – Many members of the credit union could be holding auto loans at other FIs, which can easily be identified by scrutinizing the member’s payments. Credit unions need to challenge themselves to attract these members by carving out an auto -refinance offer that is difficult to pass up! The credit union needs to do its homework well and make sure to offer rates and terms that are better and more competitive than the members’ current loans. Based on the campaigns we have run, we feel 1% lower than the member’s current rate on loans can be the magical number CUs should strive for.

- Offer extra bells & whistles to the members to sweeten the deal – This can make your auto loan product offering even more enticing than your competitors! This ‘one stop shop for all’ approach is a great way to generate considerable non-interest income too. Offering GAP and service warranties at a more affordable price point with a competitively priced auto loan is exactly what members are looking for.

- Find members with an auto loan as their next best product – Using advanced analytics and predictive models, it is extremely easy to look for triggers in a member’s behavior that can suggest whether an auto loan would be the next product for them or not. E.g., The model might suggest a member buying a house with an uptick in their salary deposits as an apt target for cross selling an auto loan.

- And lastly, do not forget to target indirect auto loan members – These members come through car dealer relationships and might not be highly engaged with your credit union. Again, advanced analytics can help identify these members that are showing a propensity to refinance their auto loans in next 6 months. This can present a great opportunity for credit unions to connect with them on an additional, direct auto loan and strengthen the relationship. This can also be a chance to cross-sell other products and services in addition to auto loans to these members.

As a credit union looking to increase the share of auto loans on your portfolio, you can decide to use one of, or a combination of the above strategies. When executed with proper data mining, analytics are bound to produce desirable results!

Trellance has launched a new Auto Refinance Program that can help you grow your auto loan portfolio by targeting your existing members who hold auto loans with other lenders. We can help you develop competitive auto refinance offers and roll them to the well-qualified members in as short as 60 days. Reach out to us today to know more about this solution.