At the start of 2023, credit unions with calendar year end financial statements were required to adopt the Current Expected Credit Loss (CECL) methodology to quantify life of loan charge offs. As credit unions get closer to the first audits of this strategy, it’s important that they understand the value of CECL back-testing and validation.

Back testing is a term used in modeling referring to the general method for seeing how well a model would have done in retrospect. For CECL, this means looking at your previous CECL calculations and comparing the amount projected with the amount of loans actually charged off. Spoiler alert: the amount held in reserve based on CECL and the amount of loans charged off very rarely match – and that’s okay. In this article, we’re going to review CECL back testing, why it’s important and what credit unions can learn from it.

CECL Back Testing: It’s okay to be Wrong

With CECL, accurately projecting future losses is ideal, but you’ll find that reasonable and supportable CECL estimates will often be wrong. So what’s the point?

First, you have to understand the reason CECL is often wrong. Say you’re flipping a coin: heads you get $5, tails you lose $5. If we apply CECL to this, the calculation would be the odds – in this case, 50% because we’re flipping a coin once and so there are 2 possible outcomes – multiplied by the amount we stand to lose, which is $5. The CECL reserve in this instance would be $2.50. That is a totally reasonable number based on the scenario – but it will be incorrect no matter the outcome, because the options are gaining $5 or losing $5.

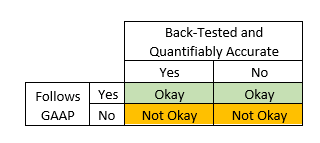

Now if we look at the numbers credit unions are actually dealing with, hundreds or thousands of loans, each of which with their own probability of being charged off, multiplied by the total amount of the loans – the numbers are going to be very different and the calculation much more complex. But so long as your credit union is following Generally Accepted Accounting Practices (GAAP), even though the amount held in reserve will likely be off, your CECL estimate is still valid.

The Value of Back Testing

Back testing CECL reserve will often prove it to be inaccurate, just like back-tested incurred loss reserve results were often inaccurate. So why back test, and why use CECL, for that matter?

CECL is a more conservative method of preparing for potential loss compared to the previous standard, the Incurred Loss methodology. CECL was created as a response to the Great Recession of 2008 and a way to ensure financial institutions were better insulated from a potential financial catastrophe.

Back testing helps your credit union get better at CECL. It allows you to look at the assumptions you made and determine if you’re being too conservative or not conservative enough. On the whole, credit unions tend to lean to the “too conservative” side of things. For many credit unions, if you were to conduct CECL back testing on what they were holding in reserve during the age of Incurred Loss, you’ll find that many were holding between 100% and 300% of what they needed. CECL back testing will allow credit unions to look at the assumptions they’re making and determine areas updates should be made.

Credit unions are still getting used to CECL. Back testing can be a great sanity check on what your credit union is currently doing or help you identify areas that should be adjusted. Back testing will continue to be important as we move forward, as it forces credit unions to consider the factors they’re including (or not including) in calculations. The economy is an ever-evolving beast – make sure your credit union is considering the changing factors that could influence how much you’ll need to hold in reserve, and that you’re periodically updating your CECL calculations to consistently have the most accurate information available.

Dan Price is the Vice President of Professional Services at Trellance.