The following is an article written by Trellance’s Vice President of Professional Services, Dan Price.

With the end of 2022 behind us, financial institutions are making predictions about economic conditions as they prepare their financial statement estimates for their annual reports. The CECL reserve is one of the most significant estimates a financial institution will make, and it is heavily influenced by the company’s economic predictions.

Predicted Economic Downturn in 2023

In their 3rd quarter earnings release, 5 of the largest US banks are predicting an economic downturn. While new loans are steadily increasing and interest income is up over last year due to the increase in interest rates, all 5 of these major banks have increased their CECL reserve in Q3, citing the economy as a major factor. Wells Fargo CEO, in his comments about the 3rd quarter, said, “We continue to see historically low delinquencies and high payment rates across our portfolios. We are closely monitoring risks related to the continued impact of high inflation and increasing interest rates, as well as the broader geopolitical risks, and while we do expect to see continued increases in delinquencies and ultimately credit losses, the timing remains unclear.”

“The overall state of the economy is deteriorating and a lot of it is just the weight of elevated inflation and higher interest rates,” said Richard F. Moody, chief economist at Regions Financial Corp. “I don’t think that we’ve seen the full effects of higher rates work their way through the economy, so that’s why we have pretty low expectations for the next several quarters.” (Cambon, 2022)

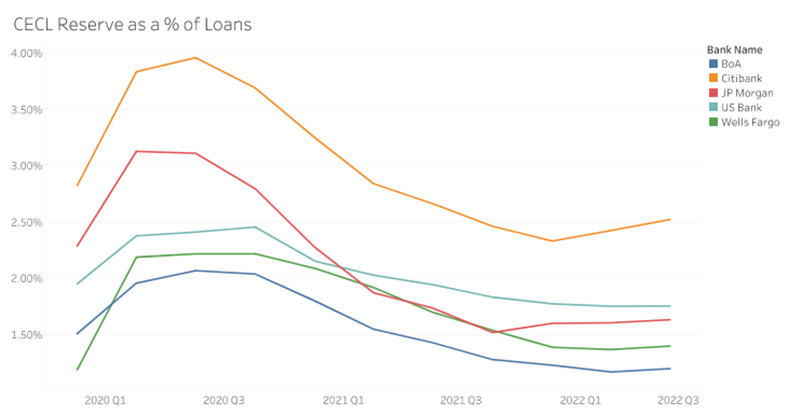

CECL Reserves Since 2020

However, none of these banks have increased their CECL reserve to pandemic levels. These reserves were significantly higher in early 2020 as banks predicted that the slowed economy would result in increased loan defaults. Government stimulus prevented (or perhaps just delayed) the economic hit. As shown in the chart below, these large banks began reversing their CECL reserves in the second half of 2020 and started increasing again in 2022.

The quarterly fluctuation in the CECL reserve is a result of the FASB requirement to assess the reserve at each reporting period and apply economic forecasts to the calculation. How much impact do these forecasts have on the final estimate? The FASB leaves this decision to management, but we can see that in practice they are having a significant impact.

In J.P. Morgan’s Q3 earnings release they attribute their 19% drop in net income from Q3 last year to fluctuations in their CECL reserve. Bank of America also reported a large reserve build-up in 2022 compared to a reserve release in 2021, “primarily driven by credit card loan growth and a dampening economic outlook”.

Factors Contributing to the Economic Downturn

Many financial institutions are using forecasts of unemployment rates and real estate values as primary drivers of their CECL estimate. Jobless claims have remained low for now, but “one of the sectors most sensitive to interest rates—housing—is showing signs of pain. Home sales posted their longest streak of declines in 15 years and the average rate on a 30-year fixed-rate mortgage eclipsed 7% Thursday for the first time in more than 20 years.” (Cambon, 2022)

Did these banks overestimate their need for large reserves in 2020, or did they just reverse them too soon? Regardless, management does appear to be more hesitant about recording those large reserves again. Will the reserves return to their 2020 high? We’ll have to wait and see.

References

Cambon, S. C. (2022, 10 27). U.S. Economy Grew 2.6% in Third Quarter, GDP Report Shows. Wall Street Journal. Retrieved from https://www.wsj.com/articles/us-gdp-economic-growth-third-quarter-2022-11666830253

Dan Price is the vice president of professional services at Trellance.