As economic uncertainty continues, credit union members are paying more acute attention to their financial situation. They are increasingly attuned to which financial products make the best sense for them – and so should the credit unions.

Gaining the insights needed to remain closely aligned with members’ needs begins with two fundamental questions:

Who are your members?

Why do they choose your credit union?

On the surface, these questions seem very simple. So simple that it’s tempting to immediately come up with the answers. However, the most successful credit unions make decisions through deep and detailed member insights that can’t be gleaned from gut instinct alone.

Advanced analytics are critical to deep and robust member understanding. Demographic segmentation is no longer enough in today’s hyper-competitive environment – you must layer it with behavioral data to bring member personas to life.

Why Your Credit Union Needs Detailed Personas

In reality, you do know a lot about your members already. But don’t make the mistake of thinking you can skip investing time and resources into persona work. Your knowledge will become much deeper and more actionable, and long-standing beliefs may be tested.

Persona research and development helps to ensure that assumptions about members are aligned with data and validated by behavior. The data analysis is performed objectively, providing internal team members the opportunity to put aside their ideas and realign around the most current facts and data.

Ultimately, arriving at an accurate and informed picture enables more personalized, meaningful member interactions while simultaneously reducing costs. Member loyalty increases, attrition decreases and risks are better understood and mitigated.

Developing Engagement-Based Member Segments

Understanding a member’s relationship with the credit union is the first step in engagement-based persona development. This means drilling into the types and number of products and services used, the number and size of transactions and the length of relationships.

To provide a snapshot understanding of a member’s relationship level, Trellance created an engagement scoring methodology that layers and weights the above factors with demographic characteristics for a succinct yet multi-dimensional view. Categorizing the information helps credit unions understand what the distinct segments look like.

Using this modeling technique with a 30,000-member credit union, Trellance created five engagement-based segments:

- Champions

- Loyalists

- Associates

- Potentialists

- Latents

Champions represent the “ideal” member. They have the highest deposits, use the most products and transact in higher amounts.

Associates, Loyalists, and Potentialists engage with the credit union, but at decreasing rates through each band. The credit union’s goal for each of these segments is to move them into higher engagement bands in a journey toward Champion status.

Latents are the least engaged members and in serious danger of attrition. The credit union now knows which members they need to target with compelling campaigns designed to reactivate and reinvigorate the relationship.

Understanding Channel Usage

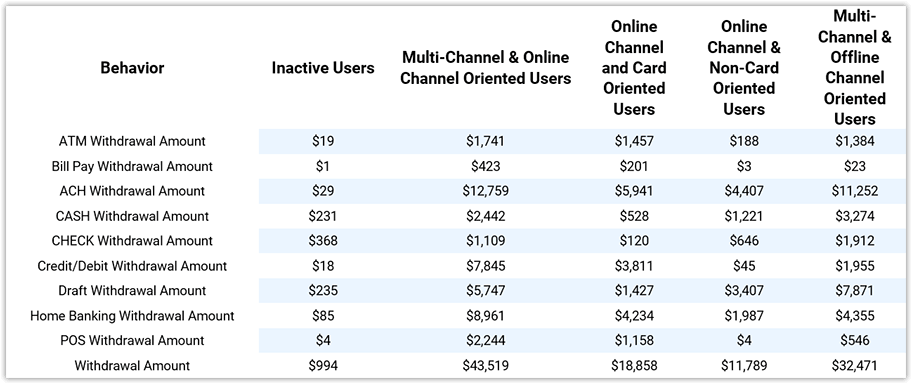

After creating engagement segments that define the relationship, an examination of daily transactional data is a valuable goldmine for further developing engagement-driven personas. Looking within POS, ACH, auto drafts and home banking transactions builds out the engagement picture more fully by identifying channel usage. This better illustrates how, when and where members interact with the credit union.

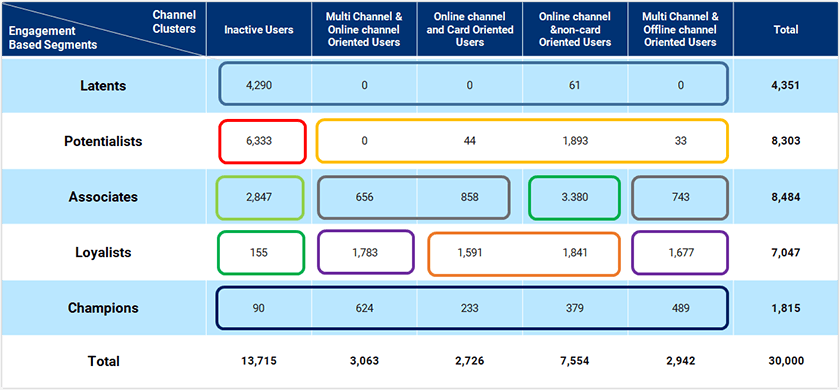

Applying a cluster analysis to members’ past transactional behavior, Trellance helped the example credit union identify channel preferences to segment its membership into five distinct clusters.

Understanding the channel usage helps the credit union connect with members in the right ways at the right moments. Using a cross tabulation technique, the channel analysis is layered on the top of engagement-based segments to build detailed member personas.

Each persona has distinct characteristics, behaviors and preferences that to the credit union can identify and cater to.

The Ultimate Engagement Persona

At the end of the process, the credit union now has a picture of nine member personas filled with insights and actionable information. For each, a vivid image has emerged built from demographics, product penetration, services, channel usage, unique characteristics and transactional behavior.

The hero archetype, Committed Cory, has more than five relationships with the credit union. On average, the Committed Corys have more than $30,000 in deposits and are actively using credit and debit cards.. At the other end of the spectrum, the Lost Lukes are defined by low deposits, transactions and engagement levels.

It should be clear that the Corys and Lukes have very different needs and require different types of outreach. With a customized marketing approach, each different persona can be communicated in a relevant and compelling way. An effective plan can be created to deepen the relationship, cross-sell and minimize potential risks.

Now, Why Do Members Choose Your Credit Union?

Though identifying why members choose your credit union seems like a logical starting place, it’s best understood after completing the persona development process. Once personas are built, each segment’s historical behavior can be analyzed to determine which factors bring them to the credit union and drive the life cycle and levels of engagement. As a member’s relationship with the credit union evolves, they can move from one persona to another. This process is known as “drift.” For the credit union in our example, Trellance defined three main factors driving persona drift:

- Cashback checking account rewards

- Short-term certificate options

- Appealing credit card offers

The credit union can now focus on three key efforts that will drive the most action. The subsequent acquisition and cross-sell campaigns will be targeted and highly effective. Even better, the credit union will save time and money by not targeting members with offers they are less likely to respond to.

Once credit unions have data-driven personas, they have made a strategic roadmap. Though the rewards are great, it’s not without challenges. Credit unions must use these detailed personas to shift their thinking away from trying to serve everyone to serving their ideal members exceptionally.

Speak with an expert

Book a meeting to discuss developing engagement-based member segments at your credit union.