Here are the Top 3 Strategies for Increasing Credit Card Profits

It’s official, Q3 of 2021 NCUA data is in. The statistics look promising for credit unions:

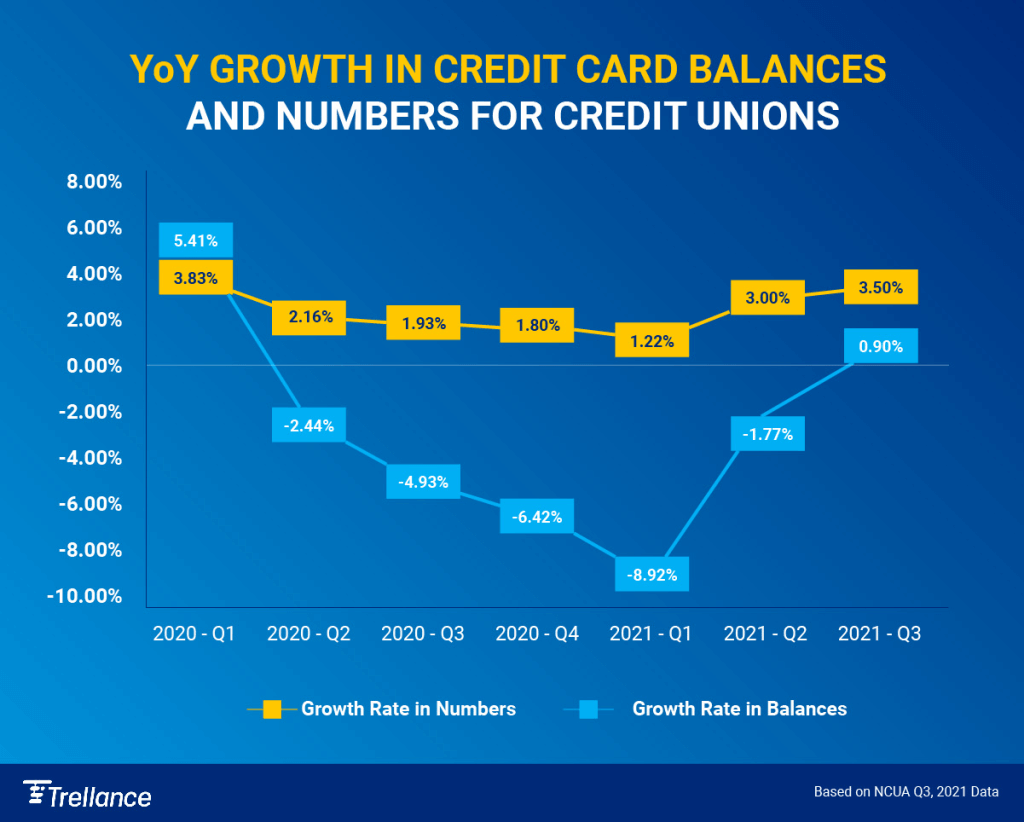

- A YoY growth in credit card balances has been recorded for the first time in the last six quarters.

- The number of cards, which was growing steadily for credit unions, also witnessed the highest YoY growth rate of 3.5% in Q3 of 2021.

We had not experienced such growth since the pandemic hit. People are eagerly returning to pre-Covid spending levels – and they want attractive credit card deals.

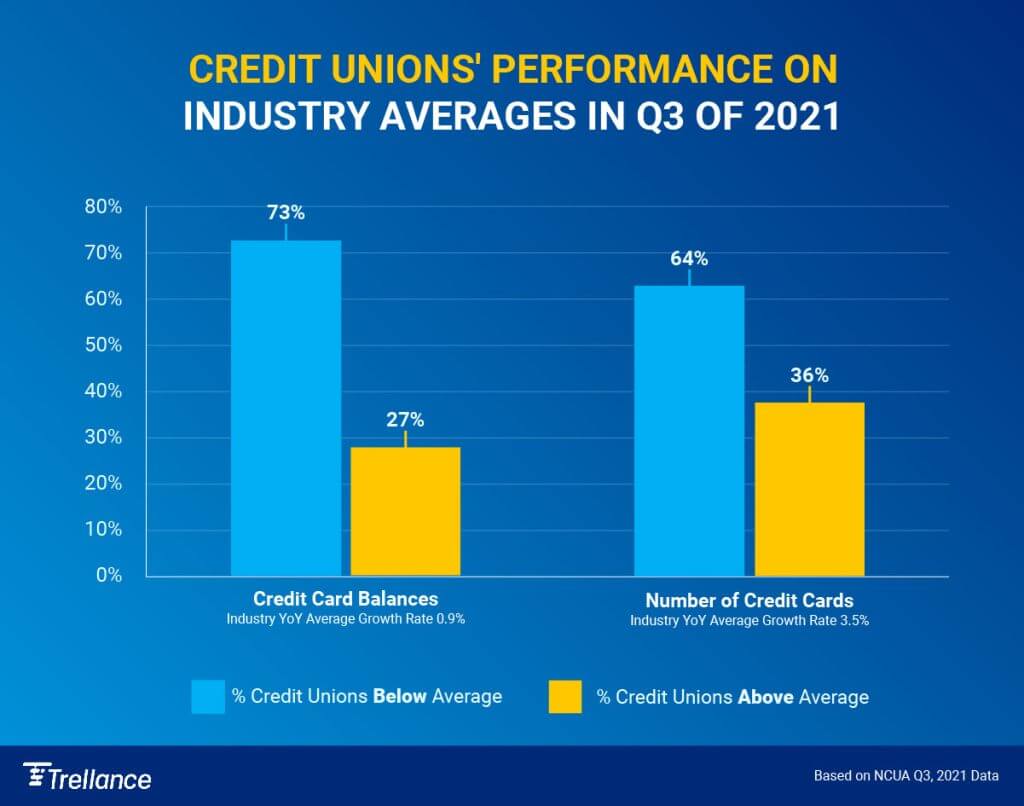

But are these positive trends enough incentive to act? Interestingly more than a third of credit unions still don’t offer a credit card program, which means they are missing easy money. And as for remaining credit unions with credit card programs:

- In Q3 of 2021, only 27% of the credit unions performed better than the YOY average growth rate for credit card balances

- And approximately 36% of the credit unions outdid the YoY average growth rate on number of credit cards

These low numbers can and should be better!

With consumer spending increasing and normalcy returning, the time is now for credit unions to approach members with credit card offers and deals that are too good to pass. So, how do we do it? These are Trellance’s Top Three Strategies:

- Roll Credit Line Increases – Use analytics to find members who can be offered credit line increases without adding to your portfolio risk. Credit line increase programs, or CLIPs, are one of the fastest ways to grow momentum in your credit card portfolio. Review member credit lines on an annual basis to ensure you are extending the proper amount of credit. If your lines are uncompetitive, it compromises your members’ engagement.

CLIPs are proven builders of loan balances and member loyalty. On average, 60% of a credit union’s credit-card-holding members are eligible for a credit-line increase, yet that opportunity remains untapped by many credit unions. For example, offering an increase to a low-transacting member who has a $2000 balance and a $5000 credit line, may incent the member to use their card more, while still managing their credit debt responsibly. Increasing your members’ credit line is a crucial strategy to keep your card top-of-mind and top-of-wallet. In addition, CLIPs are instrumental tools for increasing utilization, loans outstanding, interest and fee income. The increased spending power will not only help your members in times of need, but also will increase fees and interest income, making your program more profitable.

- Launch Balance Transfer Campaigns – It is time to get your existing and new members to stop using your competitor’s credit cards by offering competitive interest rates to roll on their credit card balances. A balance transfer should be the key ingredient to your card program. A balance-transfer program is one of the best ways to incent a member to move their balance to your card and can be promoted in several different ways. Start with encouraging your new and existing cardholders to use their credit union card to transfer balances from cards with higher rates to yours.

For example, offer a 2.99% APR for the first six months. Your lower interest rate could be the rescue they need. Create a competitive offer against national and local issuers. Position your institution as a lender that cares about its members by helping cardholders consolidate their debt. And attractive loyalty programs should be set up to offer double bonus points for the balance transfer during the promotion, without a balance transfer fee. Market the advantages of your balance-transfer program compared to competitors. Demonstrate how your balance-transfer rate is lower than others, what they can save on interest fees, and payoff timing. Also, try to tie in extra rewards points if they transfer to your card.

- Start Spending Reward Programs – Loyalty cards represent another vital component for card program growth. The top-of-wallet credit cards typically earn high-transacting members the most benefits for their loyalty. Analytics identifies those members. Your data can help validate the value and effectiveness of rewards programs in sparking transaction and revenue growth. According to creditcards.com, 57% of US adults have at least one credit card, with “cash back” being the most popular at 43%, and gas and retail coming in at 28%.

Offering cards with reward programs will increase the likelihood that your members will continually use your card. Those institutions that are using rewards programs benefit from increased transactions, greater per-transaction dollar value, and improved retention with the increase in the numbers of accounts. Rewards are not just for members but also can target employees. Every time your credit union employee assists a member enrolling for a new credit card, they can have a chance to win big through a sweepstakes portal that manages completed applications. This helps boost morale and encourages employees to sign up members for new cards.

Trellance offers more great suggestions to take advantage of a solid economy to build your credit card portfolio, but these should get you going.

Credit Card Programs Lead to Big, Easy Profit

Jump into the market with marketing programs for credit cards before your competitors do, to take advantage of this trend early on. The latest Covid variant is peaking, but consumers are not letting that deter them from spending right now. In fact, consumer spending is expected to remain strong throughout 2022. So do not be shy. Now is the time to jump in! Go aggressive on your credit card programs and let Trellance help.

Your credit card program has the potential to become one of your highest-earning assets. You can learn even more tips for increasing credit card balances and profit by checking out our White Paper: Boost Your Credit Union Profitability – Six Simple Ways to Keep Your Credit Card Top-of-Wallet.